Tips for Offering Financing to Customers

As a physician or business owner, you know that large expenses can be a significant concern for your patients and customers. Offering financing options can be an effective way to help ease the burden of a major expense or large purchase and make your services more accessible to a wider range of people. However, presenting medical or retail financing options can be a delicate matter. You don’t want to come across as pushy or insensitive to your customers’ financial situations. In this blog post, we’ll provide guidance on how to present financing options in a way that is helpful and respectful. Make Financing Options Visible When presenting your products and services, make sure to include information about financing options prominently. Display financing information on your website, in-store or in-office, and on marketing materials. This can help customers understand the financing options available and make a more informed decision about their purchase. Train + Educate Your Staff on Financing Options It’s important to ensure that your staff is knowledgeable about financing options and trained to discuss them with patients/customers. This can include providing training on the various financing options available, as well as how to discuss them in a compassionate and respectful manner. Staff members should also be able to answer any questions patients/customers may have about financing options. Provide Clear Information about Interest Rates and Repayment Terms When presenting financing options, it’s important to be transparent about interest rates and repayment terms. Make sure patients/customers understand how much they will be paying in interest and over what period of time. Also, be clear about any fees or penalties associated with late payments or early repayment. Providing this information upfront can help patients/customers make an informed decision about their financing options. Be Sensitive to Patients/Customers’ Financial Situations When discussing financing options with patients/customers, it’s important to be mindful of their financial situation. Some may be uncomfortable discussing their financial struggles, so try to create a comfortable and safe space for them to ask questions or express concerns. Also, be aware that some patients/customers may not be able to qualify for certain financing options due to their credit score or income level. In these cases, consider offering alternative payment arrangements or referring them to other organizations that may be able to provide financial assistance. Consider Partnering with a Financing Company Partnering with a financing company can offer several benefits. These companies can help simplify the financing process, allowing patients/customers to apply for financing directly through them. They may also offer promotional financing options, such as interest-free periods, which can make financing more attractive to patients/customers. Additionally, working with a financing company can help alleviate the administrative burden of managing payment plans in-house. Offering financing options can be an effective way to make your services more accessible to a wider range of patients/customers. However, it’s important to present these options in a way that is helpful and respectful. By providing clear information, being sensitive to patients/customers’ financial situations, and partnering with a financing company, you can help ease the financial burden for your patients/customers and improve their overall experience. United Credit partners with thousands of merchants to help them grow their business through financing options. We have relationships with multiple lenders, which means we have a variety of financing options to serve a wide variety of your customers. Our team is here to support you and your business every step of the way so you can focus on what matters most: your customers. Ready to get started? Begin your enrollment now. United Credit strives to keep the content shared on this blog accurate and up to date. You are urged to consult with business, financial, legal, tax and/or other advisors and/or medical providers with respect to any information presented. Opinions expressed here are the author’s alone and have not been approved or otherwise endorsed by any financial or medical institution. This content is intended for informational purposes only. Follow us on social: Linkedin-in Facebook-f Instagram Twitter

How Offering Financing Options Can Benefit Your Midwife Practice

As a midwife, you know how important it is to provide high-quality care to your patients during pregnancy, childbirth, and beyond. However, you may have noticed that some of your patients struggle with the cost of midwife services, which can lead to financial stress and even prevent them from accessing the care they need. By offering financing options to your patients, you can help to make your services more accessible and affordable, while also providing a valuable benefit to your practice. In this blog post, we’ll explore the value of offering financing options to your patients and how you can get started. Benefits of offering financing options to your patients One of the main benefits of offering financing options to your patients is that it can make your services more accessible to a wider range of patients. Many people who could benefit from midwife care may not have the financial resources to pay for it all at once. By offering financing options, you can help to remove this barrier and ensure that your patients can receive the care they need. Offering financing options can also help to build trust and loyalty with your patients. When you provide flexible payment options that work with your patients’ budgets, they are more likely to feel valued and supported by your practice. This can lead to long-term relationships and positive word-of-mouth referrals. Additionally, offering financing options can be a valuable marketing tool for your practice. By promoting your financing options on your website and other marketing materials, you can attract new patients who are looking for affordable midwife services. How to offer financing options to your patients There are a few different ways that you can offer financing options to your patients. One option is to partner with a financing company that specializes in medical financing, like United Credit. These companies can help you set up financing options for your patients, including flexible payment plans and competitive interest rates through their lending partners. Another option is to offer in-house financing, where you provide payment plans directly to your patients. While this option can be more time-consuming and may require additional administrative work, it can provide more flexibility and control over the financing options you offer. Before offering financing options to your patients, it’s important to do your research and understand the legal and financial implications. It’s also important to ensure that your payment plans are clear and transparent, with no hidden fees or surprises. Offering financing options to your patients can be a valuable way to make your midwife services more accessible and affordable, while also building trust and loyalty with your patients. Whether you choose to partner with a financing company or offer in-house financing, it’s important to do your research and ensure that your payment plans are clear and transparent. By providing flexible payment options, you can help to ensure that all patients have access to high-quality midwife care, regardless of their financial situation. United Credit strives to keep the content shared on this blog accurate and up to date. You are urged to consult with business, financial, legal, tax and/or other advisors and/or medical providers with respect to any information presented. Opinions expressed here are the author’s alone and have not been approved or otherwise endorsed by any financial or medical institution. This content is intended for informational purposes only. Follow us on social: Linkedin-in Facebook-f Instagram Twitter

What are the pros and cons of using a midwife?

When it comes to pregnancy and childbirth, there are many different options for care providers. One popular choice is a midwife, a trained professional who specializes in providing personalized care and support to women during pregnancy, childbirth, and the postpartum period. In this blog post, we will explore the pros and cons of using a midwife, the cost of midwife services, and how to explore your financing options through United Credit. What are midwifery services? Midwife services are a type of healthcare service that specializes in providing care and support to women during pregnancy, childbirth, and the postpartum period. Midwives are highly trained professionals who offer a wide range of services, including prenatal care, childbirth support, and postpartum care. They are experts in natural childbirth and focus on providing a more personalized and holistic approach to pregnancy and childbirth. Pros of using a midwife One of the main benefits of using a midwife is the personalized care and attention they provide. Midwives take the time to get to know their patients and provide care that meets their specific needs. They offer a more natural approach to childbirth, focusing on supporting the body’s natural processes rather than relying on medical interventions. This can lead to a more positive birthing experience for both the mother and baby. Another benefit of using a midwife is the lower rate of interventions and complications during childbirth. Studies have shown that women who use midwives have a lower rate of cesarean sections, episiotomies, and other medical interventions during childbirth. This can lead to a faster recovery time and a better overall birth experience. Cons of using a midwife While there are many benefits to using a midwife, there are also some potential drawbacks to consider. One of the main concerns is the lack of access to medical interventions in case of an emergency. While midwives are trained to handle many complications that may arise during childbirth, there are some situations where medical intervention is necessary. If this occurs, it may be necessary to transfer to a hospital or work with a medical doctor. Another potential drawback is the lack of insurance coverage for midwifery services. While some insurance plans do cover midwife services, many do not. This can make it more challenging to afford midwife care, especially for those who do not have the financial resources to pay for it out of pocket. Cost of midwifery services The cost of midwife services can vary depending on the location and type of services provided. On average, midwife care can, on average, cost between $2,000 and $5,000 for a standard prenatal care and vaginal delivery. However, the cost can be higher for more complex pregnancies or for those who require additional medical care. For those concerned about the cost of midwife services, United Credit offers financing options to make it more affordable. United Credit works with lending partners that provide financing options for medical services, including midwife services. Flexible payment options can help patients to pay for their midwife services over time, rather than all at once. This can help to make midwife services more accessible and affordable for patients who might not have the financial resources to pay for them upfront. Additionally, United Credit’s lending partners can offer competitive interest rates and a variety of loan options to meet the specific needs of patients who qualify. Using a midwife can be a great option for those looking for personalized care and a more natural childbirth experience. While there are some potential drawbacks to consider, many patients find that using a midwife is a positive and rewarding experience. If you’re concerned about the cost of midwife services, consider exploring financing options through United Credit. Start your application here. United Credit strives to keep the content shared on this blog accurate and up to date. You are urged to consult with business, financial, legal, tax and/or other advisors and/or medical providers with respect to any information presented. Opinions expressed here are the author’s alone and have not been approved or otherwise endorsed by any financial or medical institution. This content is intended for informational purposes only. Follow us on social: Linkedin-in Facebook-f Instagram Twitter

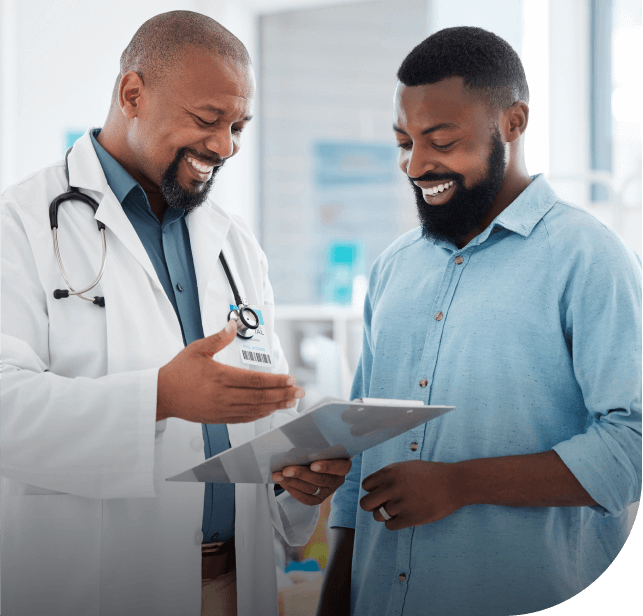

How Price Transparency Improves your Patient Experience

As a doctor, you understand the importance of providing quality care to your patients. However, quality care is not just limited to medical treatment. Patients also care about the cost of their care and having transparent pricing information can improve their overall experience. In this blog post, we’ll discuss how price transparency can improve your patient experience and the potential benefits that come with it. Builds Trust with Patients Price transparency can help to build trust with your patients. By being upfront about the cost of care, patients feel more comfortable and confident in their healthcare decisions. They can better understand the cost of treatment and plan accordingly. When patients trust their doctor, they are more likely to be satisfied with their care and have better health outcomes. Reduces Anxiety and Stress Patients can experience anxiety and stress when they receive an unexpected medical bill. By providing price transparency, patients can be aware of the cost of their care upfront and avoid any surprises. This can reduce anxiety and stress, which can improve their overall experience and satisfaction with your practice. Enhances Patient Satisfaction Price transparency can enhance patient satisfaction. When patients have a clear understanding of the cost of care, they can make informed decisions about their health. This can lead to more satisfaction with the care they receive and improved patient loyalty. Patients who are satisfied with their care are more likely to return to your practice and recommend it to others. Improves Your Practice’s Reputation Providing price transparency may improve your practice’s reputation. Patients appreciate transparency and honesty, and this can translate into positive reviews and word-of-mouth referrals. By being upfront about the cost of care, you can establish a positive reputation in your community and attract new patients to your practice. How to Implement Price Transparency in Your Practice Implementing price transparency in your practice can be a straightforward process. Here are some steps you can take to improve the transparency of your pricing information: Post Prices Online: Make sure your website includes a price list for common services and procedures. Provide Estimates: Provide patients with a clear estimate of the cost of care before they receive treatment. Explain Insurance Coverage: Help patients understand their insurance coverage and any out-of-pocket costs they may incur. Be Upfront: Be upfront with patients about the cost of care and any potential additional costs, like medication, they may face. Train Your Staff: Train your staff to communicate transparently about pricing information and answer any patient questions about costs. In conclusion, price transparency can improve your patient experience in several ways. It builds trust, reduces anxiety and stress, enhances patient satisfaction, and can lead to better overall outcomes. United Credit strives to keep the content shared on this blog accurate and up to date. You are urged to consult with business, financial, legal, tax and/or other advisors and/or medical providers with respect to any information presented. Opinions expressed here are the author’s alone and have not been approved or otherwise endorsed by any financial or medical institution. This content is intended for informational purposes only. Follow us on social: Linkedin-in Facebook-f Instagram Twitter

How Do Consumer Loans Work? (The Ultimate Guide)

Consumer loans are a type of credit that individuals can obtain to finance their personal expenses, medical procedures, or major purchases. These loans can help consumers achieve their financial goals, whether it’s getting cosmetic surgery, renovating a home, or paying for after school tutoring services. However, it’s important to understand how consumer loans work to make informed decisions about borrowing money. In this guide, we’ll explore the different types of consumer loans, how they work, and what factors to consider when deciding whether to take out a loan. Types of Consumer Loans There are several types of consumer loans, each with its own unique features and requirements. The most common types of consumer loans include: Personal Loans: Personal loans are unsecured loans that consumers can use for any purpose, such as major medical procedures, home improvements, or unexpected expenses. These loans typically have fixed interest rates and repayment terms, and borrowers must have good credit to qualify. Auto Loans: Auto loans are secured loans that consumers can use to purchase a new or used vehicle. These loans typically have fixed interest rates and repayment terms, and the vehicle serves as collateral for the loan. Home Equity Loans: Home equity loans are secured loans that consumers can use to borrow against the equity in their homes. These loans typically have fixed interest rates and repayment terms, and the home serves as collateral for the loan. Credit Cards: Credit cards are a type of revolving credit that consumers can use to make purchases and pay off over time. Credit cards typically have variable interest rates and may come with rewards programs or other benefits. How Consumer Loans Work Consumer loans work by providing consumers with access to funds that they can use for personal expenses or purchases. When a consumer takes out a loan, they receive a lump sum of money upfront and agree to repay the loan over a set period of time. Each loan has its own interest rate, which is the cost of borrowing money. The interest rate may be fixed or variable, depending on the type of loan. A fixed interest rate stays the same for the entire repayment term, while a variable interest rate may change based on market conditions. In addition to the interest rate, loans may also come with fees such as origination fees or prepayment penalties. It’s important to understand these fees before taking out a loan to avoid any unexpected costs. When a consumer takes out a loan, they agree to make regular payments over the repayment term. These payments typically include both principal and interest and are calculated based on the loan amount, interest rate, and repayment term. Factors to Consider When Taking Out a Consumer Loan Before taking out a consumer loan, there are several factors to consider: Interest rate: The interest rate determines the cost of borrowing money, so it’s crucial to compare rates from multiple lenders to find the best deal. Repayment term: The repayment term determines how long the borrower has to repay the loan, and longer terms typically result in lower monthly payments but higher total interest costs. Fees: Loans may come with fees like origination fees or prepayment penalties, so it’s important to understand these costs and the terms before taking out a loan. Credit score: Lenders may consider the borrower’s credit score when determining whether to approve a loan and what interest rate to offer. Collateral: Some loans, such as auto loans or home equity loans, require collateral to secure the loan. It’s important to understand the risks associated with using collateral before taking out a loan. Conclusion It’s also important for consumers to understand their own financial situation and budget before taking out a loan. Borrowing too much money or taking on payments that are too high can lead to financial strain and difficulty making ends meet. Consumers should only borrow what they can afford to repay and ensure that their budget can accommodate the loan payments. When shopping for a consumer loan, it’s a good idea to compare rates and terms from multiple lenders. This can help consumers find the best deal and save money on interest over the life of the loan. United Credit has a lending partner network, which offers consumers access to more financing options, more opportunities for approvals, and more peace of mind to pursue the purchases they need. In addition, consumers should read the loan agreement carefully before signing. The agreement will outline the terms and conditions of the loan, including the interest rate, repayment term, fees, and any other important details. Consumers should ask questions if they need clarification on any aspect of the loan agreement and ensure that they fully understand the terms before agreeing to them. Consumer loans can be a useful tool for financing personal expenses or purchases. However, it’s important for consumers to understand how they work and what factors to consider before taking out a loan. By comparing rates, understanding fees, and considering their own financial situation and budget, consumers can make informed decisions about borrowing money and achieving their financial goals. To explore your consumer loan options with our lending partner network, you can start an application here. United Credit strives to keep the content shared on this blog accurate and up to date. You are urged to consult with business, financial, legal, tax and/or other advisors and/or medical providers with respect to any information presented. Opinions expressed here are the author’s alone and have not been approved or otherwise endorsed by any financial or medical institution. This content is intended for informational purposes only. Follow us on social: Linkedin-in Facebook-f Instagram Twitter

What are the Benefits of Consumer Financing?

In today’s world, purchasing big-ticket items like a car or a home often requires a significant financial investment. Unfortunately, not everyone has the means to make these purchases upfront. That’s where consumer financing comes into play. Consumer financing is a loan option that allows individuals to make major purchases without having to pay for them upfront. Instead, they can make monthly payments over a period of time. In this blog post, we will discuss the benefits of using consumer financing and how United Credit can help connect consumers with the loan they need for major purchases and medical procedures. Benefit #1: Flexibility in Payment Options One of the biggest benefits of consumer financing is the flexibility it offers in payment options. This is because you can choose the repayment period that suits you best. If you opt for a longer repayment period, you’ll have lower monthly payments, which can be ideal if you have other financial obligations to fulfill. If you want to pay off your loan faster, you can opt for a shorter repayment period with higher monthly payments. This allows you to customize your repayment plan to fit your financial needs and lifestyle. Benefit #2: Easy Application Process Applying for consumer financing is often much easier than other types of loans. With United Credit, you can apply online from the comfort of your own home. The application process is simple, and you’ll receive a decision in just a few minutes. This means you can get the financing you need quickly and easily without having to go through a complicated application process. Benefit #3: Access to Higher Quality Products and Services Consumer financing can help you access higher-quality products and services that you might not have been able to afford otherwise. For example, if you need a medical procedure, but your insurance won’t cover it, consumer financing can help you get the procedure done without having to wait or settle for a lower-quality option. Benefit #4: Lower Interest Rates Consumer financing often comes with lower interest rates than other types of loans. This means you’ll pay less in interest over the life of your loan, which can save you a significant amount of money in the long run. How United Credit Can Help United Credit is a financial technology company that connects consumers and businesses with an array of experienced, innovative financing solutions. Through our lending partner network, we offer consumers access to more financing options, more opportunities for approvals, and more peace of mind to pursue the purchases they need. United Credit has a simple and easy application process. You can apply online in just a few minutes, and you’ll receive a decision quickly. Ready to get started? Begin your application here. United Credit is NOT a lender. We simply send your information to our lender network for approval and credit terms. Credit approval is not guaranteed. Please refer to our complete Terms and Conditions at: unitedcredit.com/terms-and-conditions United Credit strives to keep the content shared on this blog accurate and up to date. You are urged to consult with business, financial, legal, tax and/or other advisors and/or medical providers with respect to any information presented. Opinions expressed here are the author’s alone and have not been approved or otherwise endorsed by any financial or medical institution. This content is intended for informational purposes only. Follow us on social: Linkedin-in Facebook-f Instagram Twitter

Why should doctors and business owners offer consumer financing?

As a merchant, whether you are a doctor, dentist, or business owner, one of your primary concerns is the satisfaction of your patients or customers. This includes ensuring that they have access to the goods and services they need, without the burden of financial stress. One way to achieve this is to offer consumer financing options, such as payment plans or credit lines, that make it easier for your customers to pay for your services over time. Increase Sales and Revenue Offering financing options can help merchants increase sales and revenue. By providing more flexible payment options, you can attract a wider range of customers who may not have been able to afford your services otherwise. This means that you can tap into a larger market and generate more revenue over time. Additionally, offering financing options can increase customer loyalty, as they will appreciate the extra effort you are making to ensure they have access to the services they need. Enhance Customer Experience In today’s competitive marketplace, customer experience is more important than ever. Offering financing options can enhance the customer experience by making it easier and more convenient for customers to pay for your services. This can help reduce stress and anxiety, as customers will have more control over their finances and will not have to worry about paying large sums of money upfront. Additionally, offering financing options can help customers feel more valued and appreciated, as you are making an effort to meet their needs. Stand Out from the Competition Offering financing options can help merchants stand out from the competition. By providing more flexible payment options, you can differentiate yourself from other merchants who may not offer financing options. This can be especially important in crowded marketplaces where customers have many options to choose from. When you offer consumer financing options, you can attract customers who are looking for more convenient and flexible payment options, and differentiate yourself from competitors who do not offer such options. Support Community Health For healthcare providers, offering financing options can help support community health. By providing access to healthcare services to a wider range of patients, you can help improve overall health outcomes in your community. Additionally, offering financing options can help reduce the burden of healthcare costs on low-income patients who may not have access to traditional financing options. By supporting community health, you can build goodwill and positive relationships with your patients and the wider community. Overall, offering financing options is a win-win for both merchants and customers. Merchants can increase sales and revenue, improve cash flow, build relationships, enhance the customer experience, stand out from the competition, support community health, and increase access to goods and services. Customers, in turn, benefit from more flexible payment options that reduce financial stress and ensure that they have access to the goods and services they need. Ready to get started. Click here to enroll as a United Credit merchant. United Credit strives to keep the content shared on this blog accurate and up to date. You are urged to consult with business, financial, legal, tax and/or other advisors and/or medical providers with respect to any information presented. Opinions expressed here are the author’s alone and have not been approved or otherwise endorsed by any financial or medical institution. This content is intended for informational purposes only. Follow us on social: Linkedin-in Facebook-f Instagram Twitter

How the United Credit Merchant Portal Helps Your Business

As a merchant offering financing for medical procedures or major purchases, you want to make the process as easy and streamlined as possible for your customers. United Credit (UC) can help you do just that, with our robust merchant portal. Here are some of the benefits you can enjoy by using the portal: Real-time reporting on loan status With the UC merchant portal, you can track the status of your customers’ loans in real time. This means you can easily see which loans have been approved, which are still pending, and which have been declined. This helps you stay on top of your customers’ financing needs and ensures that you can provide them with the best possible service. Reduced paper forms The UC merchant portal eliminates the need for paper forms, which can be time-consuming and cumbersome. Instead, you and your customers can complete the entire financing process online, from application to approval. This not only saves time but also helps reduce errors and ensures that all the necessary information is captured accurately. Expedited payments With the UC merchant portal, payments are processed quickly and efficiently. Once a loan is approved, funds are deposited directly into your account within a few days. This means you can get paid faster and avoid the hassle of waiting for checks to arrive in the mail. Streamlined experience By using the UC merchant portal, you can provide your customers with a simplified experience that makes financing their medical procedures or major purchases as easy as possible. Your staff can focus on helping your customers, rather than on paperwork and administrative tasks. This can help improve customer satisfaction and drive customer loyalty and referrals. If you’re a merchant offering financing for medical procedures and major purchases, the UC merchant portal can help you provide your customers with the best possible experience. With real-time reporting on loan status, reduced paper forms, expedited payments, and a streamlined experience, you can focus on what matters most: helping your customers. If you’re a current United Credit merchant, log in to the UC merchant portal and start offering your customers the financing they need to get the care they deserve. Not a merchant yet? No problem. Apply to be part of our vast merchant network now and start funding loans for your customers in a few days. Follow us on social: Linkedin-in Facebook-f Instagram Twitter